EM Debt: Finding Fundamental Value Amid a Challenging Backdrop

While challenges remain for EM debt, technicals, in some cases, have caused market prices to overshoot their fundamental value to the downside—creating opportunities for active, bottom-up managers.

The key themes that influenced emerging markets (EM) earlier this year remain very much in place today, including war in Ukraine, inflation and a hawkish U.S. Federal Reserve (Fed), commodity price volatility and the slowdown in China’s growth. This challenging environment drove EM debt performance lower in the second quarter and caused spreads to widen even further across sovereign, local and corporate debt. The asset class also continued to experience outflows—with roughly $48.1 billion in redemptions through June 30—which exacerbated the already challenged liquidity in the market.1

However, while this has indeed been a difficult environment for EM debt, the fundamental picture is more nuanced. In particular, for active, bottom-up managers, select opportunities continue to present themselves in areas where market prices may have overreacted to the downside.

Sovereign & Local Debt: All Eyes on Fed, ECB

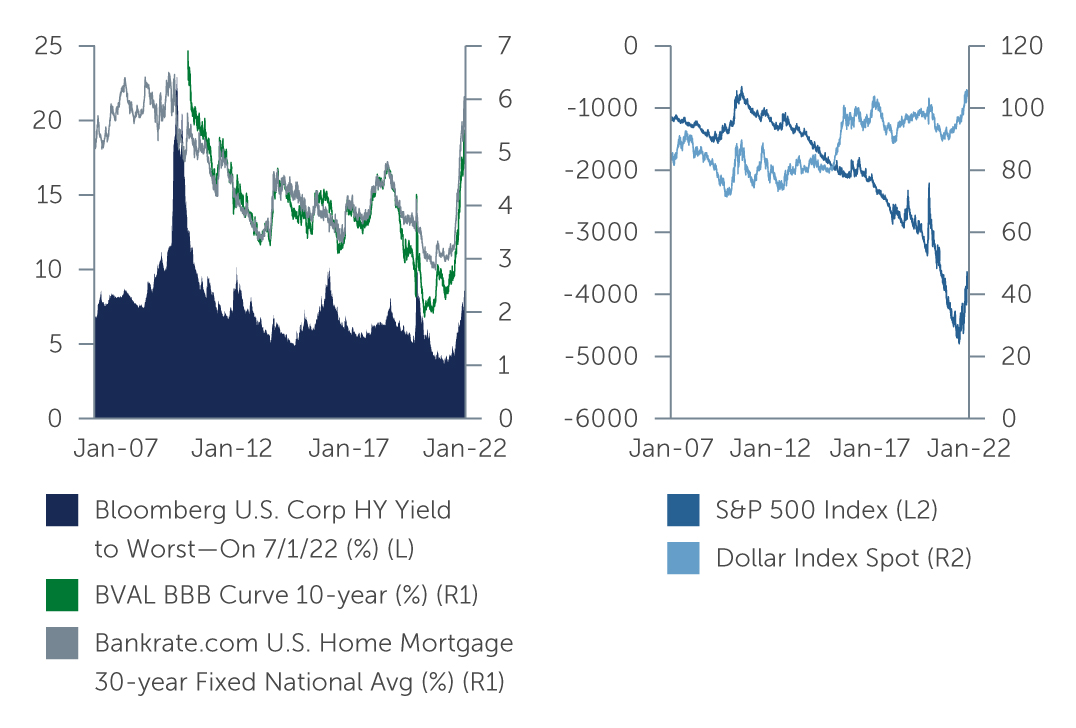

Perhaps the single biggest source of uncertainty facing EM sovereign and local debt is monetary policy, specifically the ability of the Fed and ECB to bring inflation back down to more normal levels. On the one hand, financial conditions around the world have tightened significantly, which could suggest that the Fed is closer than previously thought to reaching the end of its tightening cycle. Specifically, with a strong U.S. dollar, higher yields on both investment grade and high yield bonds, and high mortgage rates in the U.S., there is potential for demand to decrease and help ease supply-side shocks (Figure 1). There are also indications that inflation is nearing a peak, or even beginning to turn around, in certain EM countries. If we are seeing the beginning of the end of the Fed’s tightening cycle—and that’s a big ‘if’—EM local rates could start to become more attractive going forward given how much they have sold off.

On the other hand, core inflation continues to show upward movement in most countries. In many cases, the countries where rates have sold off the most—which could in theory become the most attractive opportunities—are the ones experiencing the highest inflation. Eastern and Central European countries, like Czech Republic and Hungary, are examples where inflation is in the double digits and interest rates are near 7%-8%. However, for an opportunity to fully crystallize, we would need to see more definitive signs that inflation is letting up, which has not been the case so far.

Figure 1: U.S. Financial Conditions Have Tightened

Source: Bloomberg. As of June 30, 2022.

Source: Bloomberg. As of June 30, 2022.

From a sovereign hard currency perspective, the rise in interest rates globally has been challenging, as it has increased the cost of financing. Compounding this, sustained elevated commodity prices continue to weigh on commodity and energy importers, which constitute roughly two-thirds of the EM sovereign universe.2 As a result, many countries are now facing higher current account deficits. In this environment, countries with flexible exchange rates may be better positioned, whereas those with fixed rate regimes will likely face the greatest difficulties.

At the same time, governments in certain countries are experiencing social pressure to provide relief from higher food and fuel prices in the form of subsidies. This is a factor worth monitoring, as it could remain a significant cost for countries in the near to medium term. And while this doesn’t move the needle from a credit perspective for most countries, there are a select few where the dissatisfaction with the government—and resulting pressure to increase subsidies—may start to chip away at creditworthiness.

Looking ahead, until global interest rate risks and inflation show signs of stabilizing, the environment for credit is likely to stay volatile, mainly out of concern that those risks could worsen before they get better. However, when risks do begin to stabilize, opportunities to buy oversold sovereign credit could start to emerge. Indeed, while bottom-up country selection is as critical as ever in this environment, we believe default risk in many countries is currently overpriced. Specifically, we continue to see potential opportunities in BB sovereigns such as Brazil, Paraguay and Serbia, followed by a handful of BBB and single-A countries. Very select single-Bs also look potentially attractive, but again, rigorous country selection is paramount.

Corporate Debt: Technicals Overriding Fundamentals

Similar to many other asset classes, recent market sell-offs have created significant dislocation in corporate debt prices and relegated fundamentals to the background. Indeed, the number of risks in the market, coupled with growing concerns of a recession, have created a strong risk-off tone and led to significant outflows, exacerbating the currently challenged liquidity conditions. Weaker technicals have resulted in lower primary supply compared to the last few years, with new issuance reaching roughly $159.3 billion as of second quarter end, versus $325.5 billion in the same period last year.3

On the positive side, the fundamental backdrop for EM corporates remains healthy. While higher inflation will likely create cost pressures going forward, we do not expect profit margins to suffer materially in the second half of the year—especially given that revenue and EBITDA are back to pre-pandemic levels for most issuers. Additionally, with $530.8 billion of gross funding in 2021, many corporate issuers were able to refinance a significant portion of their U.S.-dollar denominated debt at lower funding costs, which should help mitigate the effect of further Fed rate hikes. It is also worth noting that many EM corporates are commodity producers, and should continue to benefit from elevated prices. Against this healthy backdrop, the default rate for EM corporates, excluding Russia and China, is expected to remain in the low single digits, around 1-2%.4

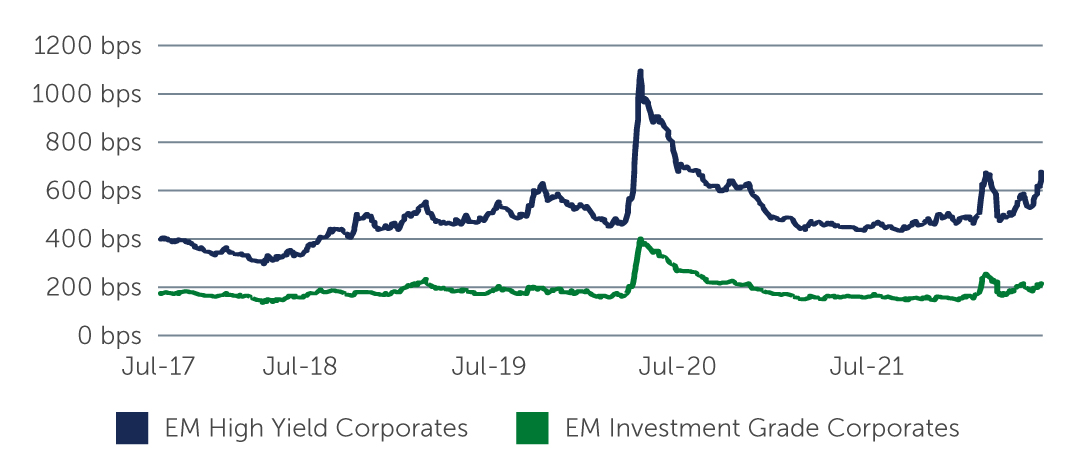

Looking at the market today, we see particular value in high yield versus investment grade corporates, as the spread differential has widened to roughly 463 basis points (bps), versus a five-year historical average of 320 bps—suggesting there is room for spread compression in certain parts of the high yield segment (Figure 2).5 This is in part due to a large portion of corporates from Russia and Ukraine, as well as a handful from Turkey and Latin America, being downgraded to high yield as a result of the risks in those countries. In some cases, outflows have exacerbated the weak technicals, causing corporate spreads to widen beyond what fundamentals would suggest—particularly given that many of these issuers are large, globally diversified EM companies—and resulted in opportunities to identify solid issuers at attractive prices. There may also be advantages to considering EM short-duration debt, which is less correlated with rate movements and therefore can provide an opportunity to pick up incremental yield and diversification, with less volatility.

From a sector perspective, there is a case to be made for being more defensive in this environment—rotating out of cyclical and lower-quality names and reducing exposure to companies with stronger reliance on the U.S. and Eurozone, particularly if the expectation is for slower economic growth, and potentially a recession, in those regions. We also continue to see opportunities in renewable power bonds. While the challenging technical picture is currently overwhelming the fundamental tailwind benefitting these bonds, we believe the strong momentum behind ESG will prove supportive over time.

Figure 2: EM Corporates IG vs. HY Spread Differential

Source: J.P. Morgan. As of June 30, 2022.

Key Takeaway

EM debt will likely continue to face challenges going forward given the sheer number of risks on the horizon. In this environment, opportunities are continuing to emerge, particularly in credits and countries where a challenging technical backdrop has caused spreads to widen beyond what fundamentals would suggest. However, as always, credit and country selection matter, and will continue to be a differentiator in performance. In our view, active managers that closely assess risk, and take a bottom-up fundamental approach to analyzing credit, will be best positioned to navigate the challenging landscape, while also identifying the areas capable of withstanding any forthcoming uncertainty.

1. Source: J.P. Morgan. As of June 30, 2022.

2. Source: Haver Analytics. As of June 30, 2022.

3. Source: J.P. Morgan. As of June 30, 2022.

4. Source: JP Morgan Corporate Default Monitor. As of May 10, 2022.

5. Source: J.P. Morgan. As of June 30, 2022.

22-2270824