Three Reasons to Consider CLOs

The combination of wider spreads, strong structural protections and low interest-rate sensitivity presents a potentially compelling case for CLOs.

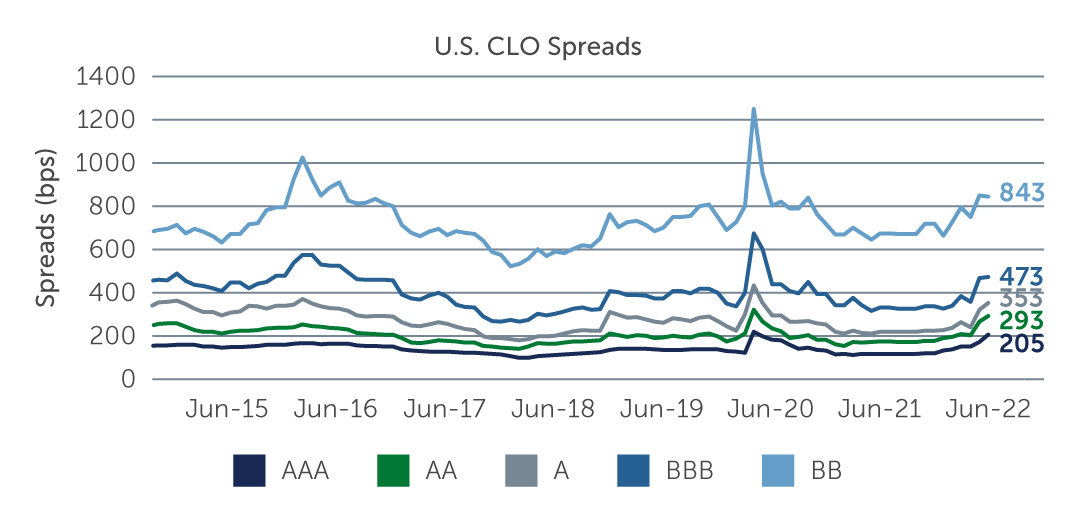

Volume and volatility are the prevailing themes in today’s collateralized loan obligation (CLO) market. In response to soaring inflation, rising rates, a war in Ukraine and growing recession fears, CLO spreads widened across all parts of the capital structure in the second quarter, in some cases significantly, and are now wide relative to both historical averages and corporate credit asset classes (Figure 1). Even with the volatility in the market, however, volume has remained steady as investors have looked to opportunistically deploy capital, and liquidity has held up fairly well. This is largely due to the development of the market over the last decade—at nearly $1 trillion in size, it is no longer a niche market, but one that has become increasingly hard for asset allocators to ignore.

Indeed, looking at the market today, there are three reasons in particular that CLOs may be worth consideration.

Figure 1: CLO Spreads Are Wide Relative to Historical Averages Source: J.P. Morgan. As of June 30, 2022.

Source: J.P. Morgan. As of June 30, 2022.

1. Wider Spreads, Potential Opportunities

The meaningful spread widening that has occurred across the CLO capital structure has created a number of potentially compelling opportunities. At the top of the capital structure, new issue spreads have widened to be more in line with secondary levels and, in some cases, are even wider. That said, we continue to see opportunities in the secondary market as well, where investors can put their money to work more quickly versus waiting for a new issue. There also tends to be more total return upside in the secondary, with opportunities to buy CLO tranches at a greater discount to par.

Further down the capital structure, secondary BBs look particularly attractive relative to new issues for short to medium-term buyers. Spreads between the two markets have experienced similar widening, but whereas new issues are generally coming to market near par, the secondary market is offering opportunities at a significant discount—with current entry points typically in the high $80s or low $90s for well-performing deals from liquid managers, and even lower for deals that have experienced some par loss or have more exposure to tail risk credits.1 Assuming that discount can be monetized as the dislocation in the market normalizes over the next 12 to 24 months, the total rate of return for buying a deal in the secondary market, versus buying a high-coupon deal at 99 or par in the new issue market, is potentially much greater over a shorter time horizon.

Of course, the relative attractiveness of any one area ultimately comes down to an investor’s risk/return profile. For longer-term and risk-based capital buyers—insurance and reinsurance companies, for instance—the new issue market, on balance, may be more compelling. Today, new issue BBs are coming to market with increased subordination levels amid expectations that economic conditions may deteriorate going forward. This added credit enhancement, coupled with the fact that these are typically clean portfolios with no tail risk credits, should help keep ratings relatively stable even through additional market stress—an important consideration for risk-based capital buyers.

Another interesting area is CLO equity, particularly new issue ‘print-and-sprint’ deals, whereby portfolios are ramped quickly (generally over a few days) in the secondary loan market at discounted levels. Many of the print-and-sprint deals pricing are structured with a 3-year reinvestment period and a 1-year non-call period. The option to call the deal opportunistically after only one year is potentially quite valuable and can translate into attractive returns from an equity perspective.

2. Robust Structures

The opportunities potentially on offer across the capital structure are in the context of CLOs’ inherently strong structures. CLO structures are notably robust, partially because they contain a series of coverage tests that protect investors’ capital over the structure’s life. An overcollateralization test, for example, diverts cash in the event a predefined ratio of collateral to liabilities dwindles low enough—thereby cutting off cash flow to junior CLO debt tranches, and instead rerouting it to senior debt tranches. An interest diversion test, which is a similar concept, instead reroutes cash to buy more collateral. By paying down the structure or enhancing its collateral value, the mechanisms are effectively offsetting some of the effects of defaults and trading losses.

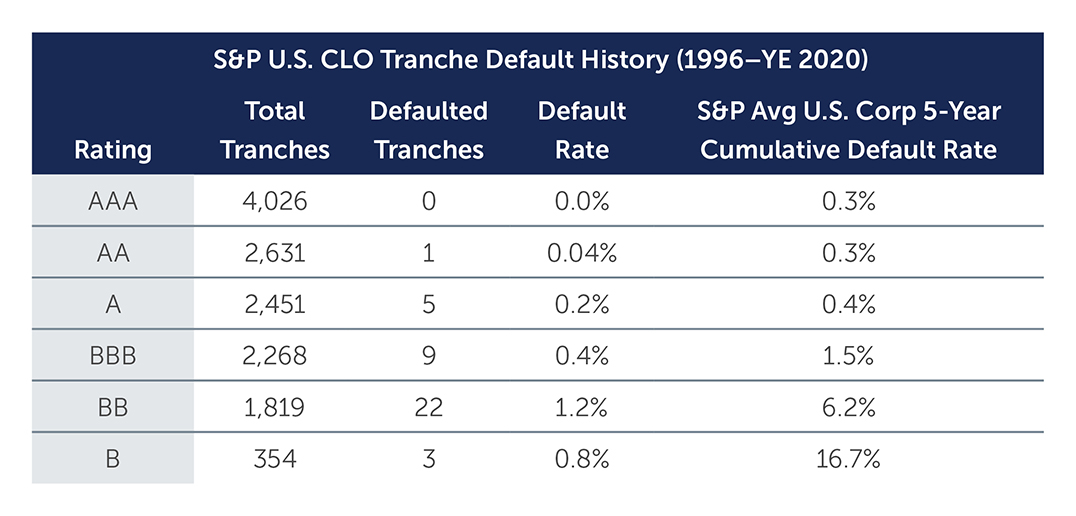

As a result of these resilient structures, CLOs have weathered past periods of stress relatively well. CLO tranches have defaulted far less frequently than equivalently rated corporate credit and other securitized products, reinforcing the attractiveness of the asset class versus traditional fixed income sectors. In fact, no AAA tranches have ever defaulted or experienced a principal impairment (Figure 2). Further down the capital structure, BBs have historically had a default rate of less than 2%. Even if we see a near-term uptick in the underlying loan defaults going forward, we expect them to remain below or in line with historical averages of 2.5% to 3%—CLO structures would still be well within the realm of what they are built to withstand.

Figure 2: CLO Tranches Have Defaulted Less Frequently Than Similarly Rated Corporate Credit Source: S&P. As of December 31, 2020.

Source: S&P. As of December 31, 2020.

That said, within CLOs, we are also keeping a close eye on downgrades to the underlying collateral. While our base case scenario is not for a swathe of downgrades like we saw in early 2020, there is concern that loan market weakness will lead to downgrades from single-B rated loans to CCC rated loans. If the percentage of CCCs within the underlying collateral increases to the point that it’s nearing the typical 7.5% threshold, then haircuts will be applied in the calculation of the coverage tests, which could trigger the structure’s cash diversion mechanism and cut off cash flows to the junior debt tranches. However, it’s worth noting that CCCs, on average, currently make up only about 3%–4% of CLOs’ underlying collateral. On top of that, CLOs currently have an additional cushion of about 3%–4% between their actual over-collateralization amount and their required over-collateralization level, which should offer some degree of comfort heading into a more challenging period.

3. Low Interest Rate Sensitivity

The case for CLOs is amplified by the asset class’ floating-rate nature. CLOs offer floating-rate coupons, which means that as interest rates rise, CLO coupons increase accordingly. This effectively lessens duration, or interest rate risk, over time. As a result, relative to fixed rate asset classes like high yield or investment grade corporate bonds, prices on CLOs have historically been more stable in rising-rate environments. Amid expectations that the U.S. Federal Reserve will continue interest rate hikes going forward, with likely significant increases on the horizon, the floating-rate nature of the asset class positions it on potentially solid footing and increases the likelihood that it will benefit from continued strong demand.

Takeaway

CLOs have not been immune to the recent market volatility, and expectations for economic weakness going forward are certainly cause for caution. However, we believe CLOs have adequate structural protections to weather the storm and current valuations offer an attractive opportunity to add risk. Active management is critical, as CLO managers are responsible for selecting and monitoring the underlying loan managers. At Barings, we look for loan managers with experience managing through multiple cycles and periods of economic stress, a track record of minimizing credit losses, a deeply resourced team, strong internal research capabilities and consistency of style. This is essential to navigating volatile environments, and to both minimizing potential risks and capitalizing on relative value as it emerges up and down the capital structure.

1. Source: Barings’ market observations. As of June 30, 2022.

22-2268807