Multi-Asset Insights: War Gaming

Energy shocks and geopolitical risk are driving volatility across markets, but uncertainty also creates opportunity. With sentiment and valuations showing signs of dislocation, we see scope to move cautiously beyond core positioning as fundamentals remain broadly constructive.

Executive Summary

- For several months, our Multi-Asset Team has managed portfolios conservatively in anticipation of rolling bouts of volatility caused by economic dispersion and geopolitical aggression

- Full valuations, crowded positions and the accumulation of uncertainty ultimately create market dislocations that allow investors to “play more offense” in seeking out returns

- The ongoing war in Iran has created some dislocations with significant impact on energy markets and short-term inflation expectations

- Stagflationary shocks are particularly challenging to manage because of the dual hit to both risk assets and the risk-free interest rate markets

- The aggressive repricing of sovereign yields in March has opened up pockets of value across the U.S., Europe, U.K. and LatAm

- Having approached markets from a place of conservatism, the Multi-Asset team now sees merit in beginning to add risky asset exposures in credit and equities at current valuations

- Across credit and equities, we prefer the U.S. over Europe given Europe’s more challenging growth, inflation and policy backdrop

March Madness

“Plans are of little importance, but planning is essential.” That is one of the many timeless quotes attributable to Winston Churchill, and few leaders of the last century faced the uncertainties and consequences of war more directly than the late prime minister. His wise words resonate today as global powers scramble to chart a course for the ongoing war in Iran, and as investors and markets hustle to assess the fallout.

And while the latter half of Churchill’s quote highlights the need for forward-looking perspectives, the beginning almost perfectly captures the somewhat unprecedented dynamic of today’s news flow: any well-laid plan can be completely upended by a single “tweet” at any moment.

Setting the Scene

In our most recent Multi-Asset Markets Call, held coincidentally a few days before the war in Iran began, we made the case for positioning multi-asset portfolios more cautiously for the near-term. For several months, the Multi-Asset teams has argued that investors should prepare for heightened bouts of volatility as the world manages increasingly polar economic outcomes, exacerbated by more aggressive approaches to policy and geopolitics.

Greater economic and policy uncertainty alone can justify a higher bar for risk-taking. Reinforcing the case for conservatism was the combination of crowded positioning and lofty valuations across asset classes. Coming into 2026, we saw credit spreads near all-time tights, historically elevated P/E ratios in equities, rates markets pricing in several more Fed cuts, and robust optimism for emerging markets. When sentiment and pricing are this exuberant (or complacent), it takes little disruption to generate losses.

As a result, our approach over the last couple months has been to hunker down and build portfolios around the highest-quality, lowest-volatility assets (“Stabilize Your Core”); to allow the chaotic mix of economic dispersion and policy/geopolitical disruption to shake sentiment and create some selling of levered positions; and ultimately to use volatile dislocations across markets to construct well-balanced multi-asset portfolios at better valuations with improved technical conditions.

As we will highlight below, the ongoing war in Iran has created a number of dislocations across markets, giving investors the opportunity to start carefully moving beyond the “cautious core” to pick up assets at more attractive prices.

Fallout from the War in Iran

While conservative positioning has felt better than the alternative the last few weeks, stagflationary risks from the war in Iran have left very few places to hide. A spike in global energy prices is putting inflation risk front and center for global sovereign interest rate markets. West Texas Intermediate and Brent crude oil have both spiked over 50%, and European natural gas prices are up over 70%, more than 100% from their January lows. The International Energy Agency (IEA) is calling this war the "largest energy shock ever," with roughly 12–15% of global oil supply potentially being removed from the market with serious risk of oil reaching $150 per barrel in the weeks ahead.

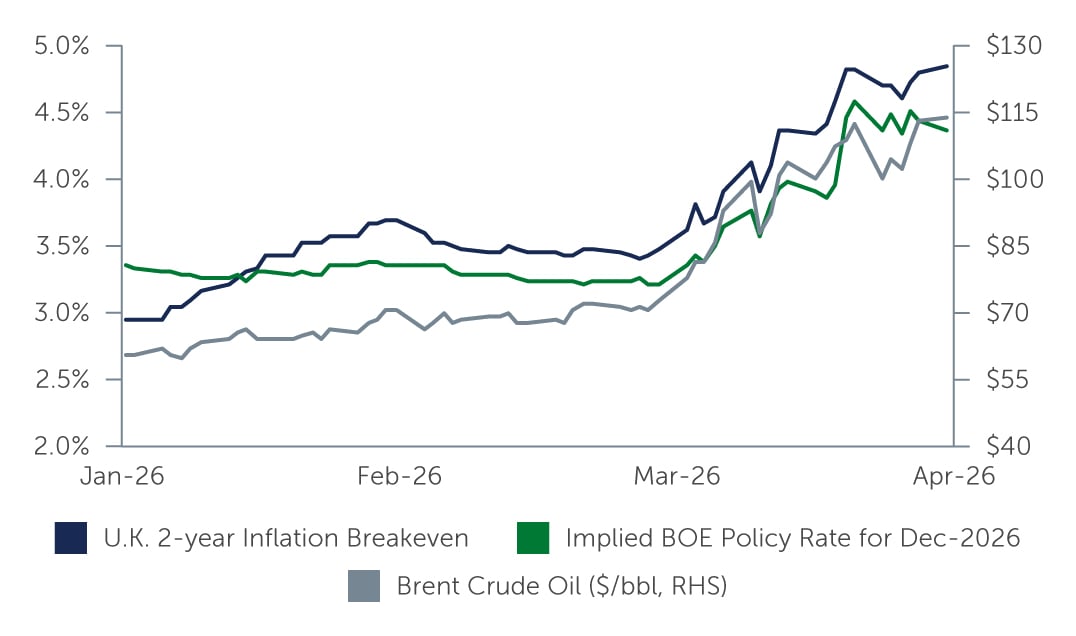

With the effects of this energy shock being felt immediately in every sector of the economy, two-year inflation breakevens in the U.S. have risen 100 basis points (bps) year-to-date, while two-year breakevens in the U.K. have risen over 180 bps. This aggressive re-pricing in inflation markets has whipsawed expectations for central bank policy. At the end of February, the market was pricing in two 25 bps cuts from the Bank of England (BOE) this calendar year; just one month later, the market is pricing in three 25 bps hikes, a stunning reversal in expectations. While less dramatic, the pricing of the U.S. Federal Reserve (Fed) policy has swung from 2.5 cuts for 2026 to no cuts at all, still a substantial change in policy perspective.

Figure 1. Oil, Inflation & Central Bank Pricing

Source: Bloomberg. As of March 30, 2026.

Source: Bloomberg. As of March 30, 2026.

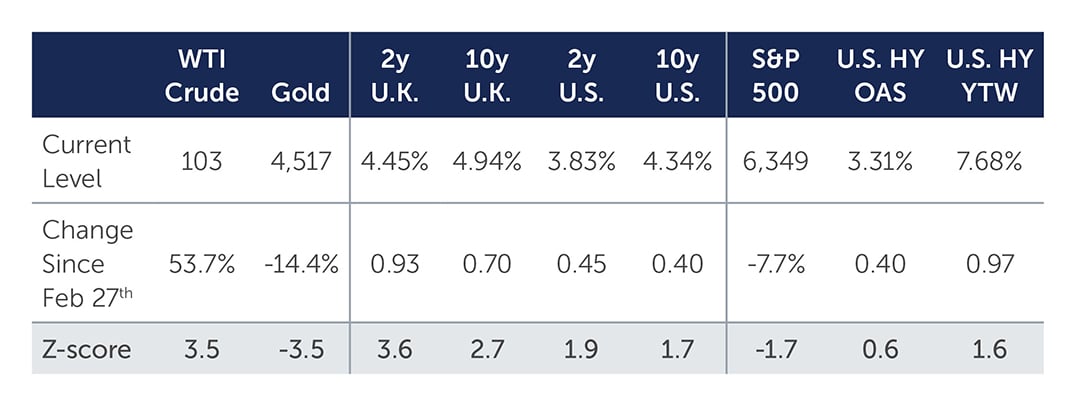

The swing from pricing rate cuts to rate hikes has pushed front-end sovereign yields dramatically higher. In the U.K., two-year yields have had a 3.6x standard deviation move in March, rising a full 105 bps. The U.S. has seen a dramatic bear flattening move with front-end yields up more than 50 bps from the February lows and 30-year yields testing 5.0% for the first time since last July.

Figure 2. Cross-asset Market Moves

Source: Bloomberg. As of March 30, 2026.

Source: Bloomberg. As of March 30, 2026.

The move higher in risk-free yields has played an important role in the relative performance of equity and credit markets. The S&P 500 is down -7.3% as of March 30, 2026 since the war began1, while U.S. high yield (HY) bond spreads have only widened 40 bps. Historically, a -5% drawdown in the S&P 500 has tended to coincide with an approximate 75 bps of widening in high yield credit spreads, in this instance implying 110 bps of spread widening.

We have seen a similar dynamic in investment grade (IG) credit, where index-level spreads are just 10 bps wider in March, outperforming IG’s typical beta to both equities and HY spreads.

A huge factor here is the demand from “yield buyers”. With the backup in the sovereign risk-free component, the index level yield in U.S. HY has risen 97 bps up to 7.7% since February 27, 2026, a yield level that meets the target returns of many institutional investors. Higher Treasury yields tend to exacerbate the sell-off in equity markets, but these higher yields are also cushioning some of the spread widening in credit.

While the equity market has dealt with “fast money” players—like hedge funds and CTAs—aggressively hedging and de-grossing risk, this accordion-like interplay between rates and spreads in credit speaks to a structural demand for income among institutional and retail investors alike. This is a key factor shaping how valuations evolve in moments like these.

How Do We Assess the Likely Outcomes from Here?

When considering the scenarios and incentives for the war going forward, we have two dramatically different perspectives on the opposing sides. We begin with the U.S.

On one hand, there is clear seriousness behind the Trump administration’s desire to permanently impair Iran’s ability to possess nuclear capabilities or long-range ballistic missiles. With President Trump now in his second term, the political calculus is less influenced by short-term outcomes than it otherwise might be, especially for an administration that seems intent on leaving a long-lasting imprint on the world’s geopolitical order.

However, the 43% increase in prices at the pump since February 27, 2026 is certainly a pressing economic and political reality, as is the deployment of thousands of American soldiers to the Gulf for an administration whose campaign emphasized tackling inflation and keeping troops out of harm’s way. As evidenced by the optimistic posts on Truth Social following particularly difficult market days, our base case is to start positioning for an “off-ramp” from the Trump administration as the difficulties of today’s headlines start to compete with the appeal of longer-term legacy projects.

On the Iranian side, there is an existential threat at play in understanding the regime’s incentives, but that doesn’t mean the calculus is entirely one-sided. While the power of the religious and survivalist influences can’t be underestimated, creating an incredibly high tolerance for pain, Iran is not immune to economic or political realities. As summer draws nearer, the intense heat in the region creates a significant demand for fiscal support for necessities including water and food, and the funding for that fiscal spending comes almost entirely from oil revenues.

It is notable that China, a key ally of Iran’s in recent history, has so far offered a muted response to the war. We see this as reflecting two perspectives: one, China has built up at least three months’ worth of strategic petroleum reserves; and two, the more impactful development for China may be a peaceful outcome in the economic and trade “war” with the U.S., particularly around semiconductor supply chains.

From our perspective, the delay of President Trump’s visit to Beijing until mid-May displays China’s willingness to allow time for the U.S. to find that off-ramp in Iran. Taken together with an Iranian regime already facing domestic upheaval and confronting the military might of a growing list of opposing countries, we see the most likely scenario as a contained ceasefire. Under this outcome, Iran would maintain control over the Strait of Hormuz, so long as transport is allowed to continue in a reliable way. As we noted at the outset, we will be constantly revisiting this assessment.

How Do We Align the Potential Outcomes with Opportunities in the Market Today?

While our base case is for a two-sided resolution in the days and weeks ahead, we are incredibly mindful of downside scenarios. Deterioration from here likely involves heavy attacks on energy infrastructure that could keep oil prices well over $100 per barrel for months or quarters, which would also likely necessitate putting troops “on the ground” in active warfare. This would be incredibly disruptive for sectors exposed to inputs traveling through the Strait of Hormuz and would be particularly inflationary for Europe.

However, even in a drawn-out conflict with oil above $100 for another three to six months, our economics team has estimated the GDP impact in the U.S. to be less than 50 bps, with a 40 bps bump to core inflation. While that stagflationary evolution is uncomfortable, it is not on the scale of the type of macro shock that would drive a sustained bear market for risky assets, especially with a corporate sector that was otherwise showing signs of a solid cyclical uplift and with rates markets already pricing in a full reversal of central bank policy, which we see as unlikely.

The backdrop is not as rosy for Europe which already had less cyclical support and where both the growth and inflation impacts from this war are more harmful. Our preference is to favor U.S. risky assets over Europe as we start to extend beyond the lowest-volatility core assets to add new positions in multi-asset portfolios in U.S. credit across both IG and HY. Similarly, we like cautiously adding back U.S. equity exposures across both tech-oriented sectors and small caps where the earnings outlooks are still quite robust for 2026.

In terms of hedging, risky asset hedges like the VIX or credit CDX have become less attractive given their expensive levels. Instead, we prefer a mix of USD and real rates as a ballast to multi-asset portfolios today. As for nominal interest rates, the dramatic re-pricing of central bank policy paths is starting to look like a “dislocation”, but we should acknowledge that the inflation data will be very elevated for at least the next couple of months, especially in Europe.

While Fed Chair Powell just reiterated “the tendency is to look through any kind of a supply shock” if long-run inflation expectations remain anchored, the BOE and European Central Bank (ECB) must wrestle with maintaining credibility in the face of a more challenging inflationary trajectory in the months ahead. In our mind, some humility that central bank policy cannot affect the flow of oil through the Strait of Hormuz would make it more likely that developed market central banks keep policy rates on hold through the summer rather than embark on a sustained rate hiking cycle. Our preference is to make careful bets in the risk markets first, and await more clarity on the path of inflation and broader economic growth before really leaning into duration across U.S. and Europe, although valuations are quite appealing today both in terms of the implied path for policy rates and the term premia offered out the curve.

Conclusion

The dynamics in Iran present an incredibly difficult challenge: first, because the incentives of the actors involved are not purely economic; and second, because the most direct impacts are concentrated in energy and commodity markets, driving an immediate rise in inflation and causing a wholesale sell-off across the entire capital stack. In these moments, humility and discipline are critical to successful multi-asset portfolio management, but we also have to keep in mind that uncertainty is the very thing that creates opportunity for risk-taking.

We still see a macro backdrop that is largely constructive for the corporate sector, supporting investment returns over the year ahead. However, as we have noted for the last few months, we also anticipate more volatility than in years past, whether caused by disruptions from AI or by more aggressive geopolitical agendas. In periods of heightened unpredictability, the discipline embedded in our process has kept us conservatively positioned through the first quarter of this year.

Now that sentiment, positioning and valuations are starting to show signs of dislocation, we favor extending beyond our core multi-asset portfolios for new positions in risky asset exposures, particularly in the U.S. As we move forward, we recognize that the plans may need to evolve, but the discipline and the process behind the planning are essential.

1. Measured from 2/27/26 close to 3/30/26 close

26-5353463