Any forecasts in this material are based upon Barings opinion of the market at the date of preparation and are subject to change without notice, dependent upon many factors. Any prediction, projection or forecast is not necessarily indicative of the future or likely performance. Investment involves risk. The value of any investments and any income generated may go down as well as up and is not guaranteed by Barings or any other person. PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

Any investment results, portfolio compositions and or examples set forth in this material are provided for illustrative purposes only and are not indicative of any future investment results, future portfolio composition or investments. The composition, size of, and risks associated with an investment may differ substantially from any examples set forth in this material No representation is made that an investment will be profitable or will not incur losses. Where appropriate, changes in the currency exchange rates may affect the value of investments. Prospective investors should read the offering documents, if applicable, for the details and specific risk factors of any Fund/Strategy discussed in this material.

Barings is the brand name for the worldwide asset management and associated businesses of Barings LLC and its global affiliates. Barings Securities LLC, Barings (U.K.) Limited, Barings Global Advisers Limited, Barings Australia Pty Ltd, Barings Japan Limited, Baring Asset Management Limited, Baring International Investment Limited, Baring Fund Managers Limited, Baring International Fund Managers (Ireland) Limited, Baring Asset Management (Asia) Limited, Baring SICE (Taiwan) Limited, Baring Asset Management Switzerland Sarl, and Baring Asset Management Korea Limited each are affiliated financial service companies owned by Barings LLC (each, individually, an “Affiliate”).

NO OFFER: The material is for informational purposes only and is not an offer or solicitation for the purchase or sale of any financial instrument or service in any jurisdiction. The material herein was prepared without any consideration of the investment objectives, financial situation or particular needs of anyone who may receive it. This material is not, and must not be treated as, investment advice, an investment recommendation, investment research, or a recommendation about the suitability or appropriateness of any security, commodity, investment, or particular investment strategy, and must not be construed as a projection or prediction.

Unless otherwise mentioned, the views contained in this material are those of Barings. These views are made in good faith in relation to the facts known at the time of preparation and are subject to change without notice. Individual portfolio management teams may hold different views than the views expressed herein and may make different investment decisions for different clients. Parts of this material may be based on information received from sources we believe to be reliable. Although every effort is taken to ensure that the information contained in this material is accurate, Barings makes no representation or warranty, express or implied, regarding the accuracy, completeness or adequacy of the information.

Any service, security, investment or product outlined in this material may not be suitable for a prospective investor or available in their jurisdiction. Copyright in this material is owned by Barings. Information in this material may be used for your own personal use, but may not be altered, reproduced or distributed without Barings’ consent.

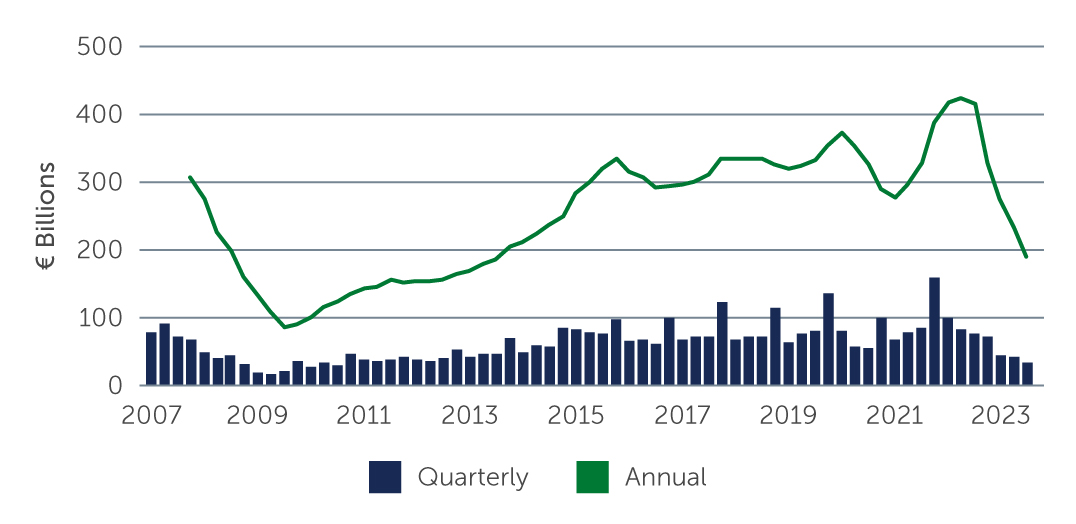

Source: Real Capital Analytics/MSCI. As of September 30, 2023.

Source: Real Capital Analytics/MSCI. As of September 30, 2023.