Re-Rating Korea: A Structural Case for Korean Equities

Korean equities rallied strongly in 2025 and have extended those gains into this year, placing the market firmly on global investors’ radar.

Demand linked to AI and advanced technology has been the primary driver, supported by resilient sentiment around AI and a meaningful earnings tailwind for semiconductor companies.

Yet the story is not just about technology. A range of factors is also supporting a more structural investment case for Korea, including improving corporate governance, a more shareholder-friendly policy direction, and a broader set of opportunities beyond tech. At a time when global equity leadership is increasingly concentrated, this is opening up a more differentiated opportunity set for investors.

Technology Leadership in an AI-Driven World

A Market at the Core of Global Innovation

Korea occupies a strategic position in the global technology ecosystem, underpinned by its leadership in memory semiconductors. Samsung Electronics and SK Hynix remain dominant players, and as of last year the two companies together accounted for roughly 70% and 50% of global DRAM (Dynamic Random Access Memory) and NAND (NAND Flash Memory) revenue, respectively1. These technologies are fundamental to AI-driven computing, with DRAM enabling high-speed processing and NAND supporting large-scale data storage.

As cloud infrastructure, hyperscaler investment, and data-intensive AI workloads continue to scale, demand for memory is becoming increasingly structural rather than cyclical. In the emerging era of agentic AI, the importance of memory is rising further, as it enables systems to retain context, leverage prior interactions, and support more coherent multi-step reasoning and decision-making. This is particularly evident in high-bandwidth memory, where rising memory intensity per server is driving demand for more advanced solutions. As a result, memory is becoming less tied to traditional end markets such as PCs and smartphones and more central to the long-term buildout of digital infrastructure. This shift is improving earnings visibility and reinforcing Korea’s role in the AI value chain.

At the same time, the commercial profile of the memory market is evolving. Tighter supply conditions, longer-term customer agreements, and increased AI-related content are contributing to a more durable demand backdrop and improved pricing visibility for leading suppliers.

Momentum is also extending beyond memory into adjacent segments, including semiconductor equipment, materials, display technologies, and battery-related industries, where Korea plays an important role across the value chain. As a result, Korea’s technology leadership is no longer confined to a narrow group of companies, but is developing into a broader structural growth theme supported by sustained AI-driven investment and ongoing technological upgrading.

Figure 1: Accelerating AI Adoption Boosts Memory Demand

Source: WSTS, J.P. Morgan estimates, March 22, 2026. E = Estimates

Source: WSTS, J.P. Morgan estimates, March 22, 2026. E = Estimates

From Governance Discount to Re-Rating Opportunity

The Significance of “Value-Up”

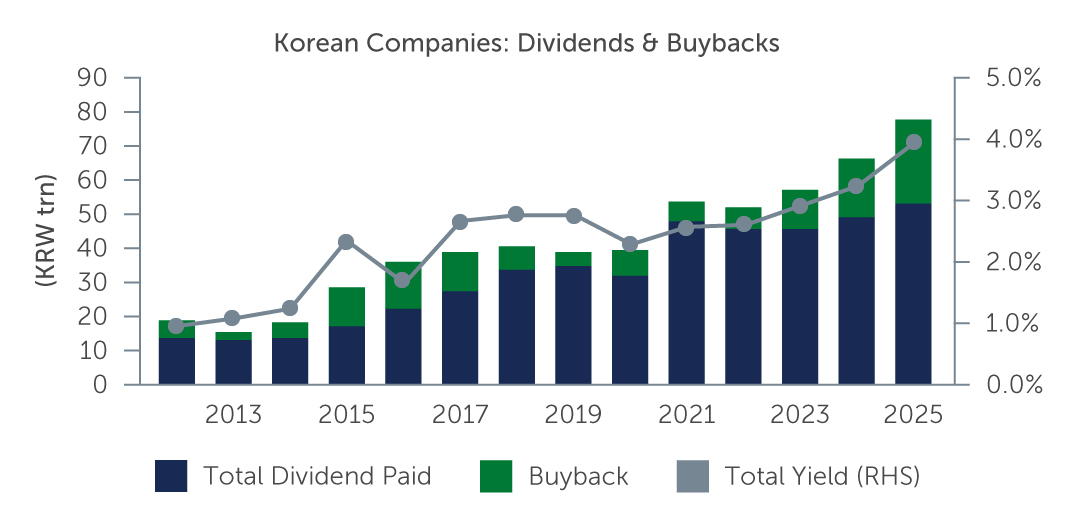

A defining feature of the Korean equity market has been its persistent valuation discount relative to global peers. This reflects structurally low returns, conservative capital allocation, complex ownership structures, and limited shareholder engagement—despite strong industrial competitiveness.

The government’s Value-Up initiative, launched in 2024, is a meaningful step toward addressing these inefficiencies. Alongside revisions to the Commercial Act—aimed at strengthening board accountability and fiduciary oversight—it reinforces minority shareholder rights, improves corporate governance, and encourages clearer capital allocation and shareholder return policies, helping address the long-standing Korea discount.

Recent measures further support this direction. Tax incentives are encouraging higher dividends, while legal changes provide stronger support for shareholder-friendly actions such as treasury share cancellations. Although still early, signs of progress are emerging, with more companies raising payouts, conducting buybacks, and improving capital allocation, particularly in the financials and industrials sectors.

In a market long defined by discount, even incremental improvements in capital discipline can support meaningful valuation upside. As investors increasingly reward stronger shareholder alignment, the basis for a broader re-rating should strengthen over time.

Figure 2: Rising Trend of Total Shareholder Return Yield for Korean Companies Supported by Increasing Dividends and Buybacks

Source: FactSet, Goldman Sachs Global Investment Research, May 31, 2026. Based on KOSPI companies.

Source: FactSet, Goldman Sachs Global Investment Research, May 31, 2026. Based on KOSPI companies.

Beyond the Headlines: A Broader Opportunity Set

Expanding Themes Across Industrials & Domestic Sectors

Investor attention often centers on a small number of large-cap technology companies. While these names remain important anchors for the Korea market, that narrow focus can obscure the breadth and evolving nature of the opportunity set.

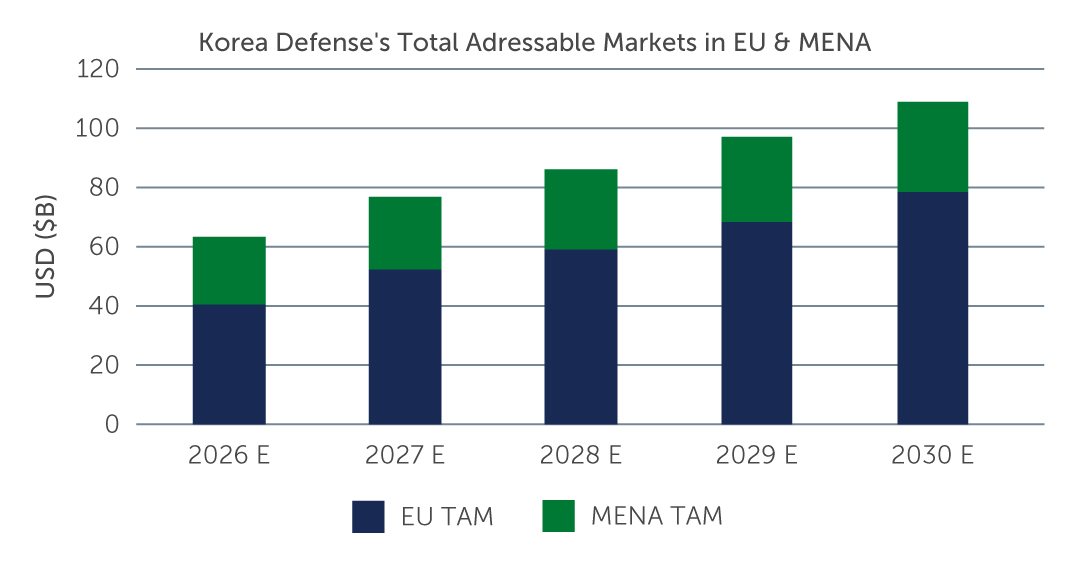

Within Industrials, Korea is benefiting from shifts in global supply chains, as geopolitical considerations drive a greater emphasis on resilience, localization, and strategic partnerships. In this context, Korea is emerging as a key manufacturing and export hub, particularly within US-aligned supply chains.

This is translating into rising demand across sectors such as defense, shipbuilding, power infrastructure, and energy storage, alongside continued growth in factory automation and robotics. These industries are increasingly tied to long-term themes, including the evolving global security landscape, U.S. re-industrialization, the energy transition, infrastructure modernization, and strategic supply chain resilience, supporting more sustainable growth.

Figure 3: Korea’s Defense Seeing Order Visibility in EU & MENA

Source: Military Balance, International Monetary Fund, SIPRI, J.P. Morgan estimates, April 20, 2026. TAM = Total Addressable Markets. E = Estimates

Source: Military Balance, International Monetary Fund, SIPRI, J.P. Morgan estimates, April 20, 2026. TAM = Total Addressable Markets. E = Estimates

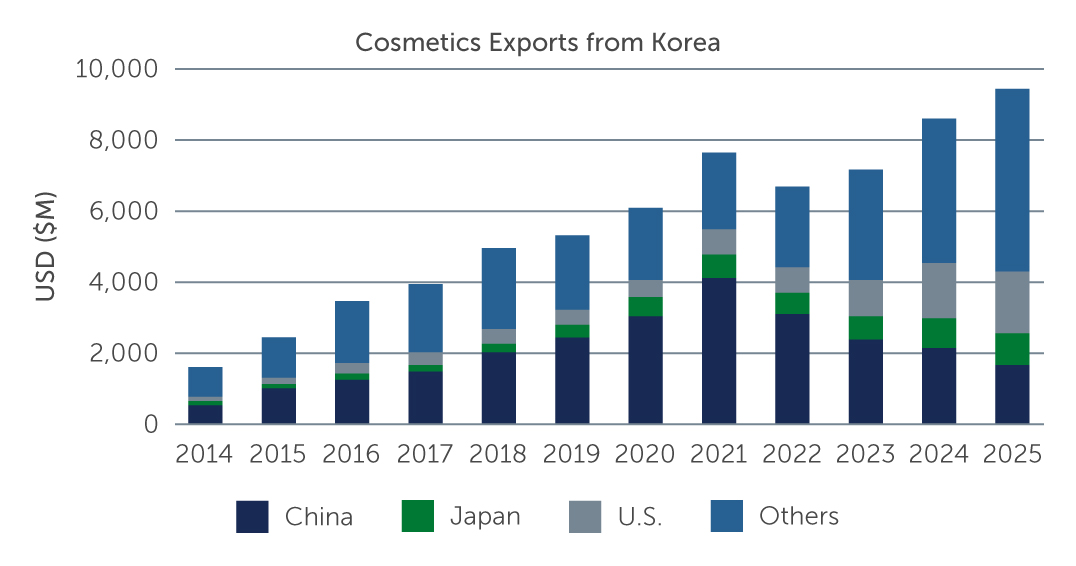

Beyond industrials, Korea also offers differentiated opportunities across consumer and health care sectors, supported by the global expansion of Korean popular culture (K-culture). Areas such as medical aesthetics, cosmetics, biopharmaceuticals, and entertainment are benefiting from the internationalization of Korean brands and intellectual property, with companies generating an increasing share of revenues overseas.

Figure 4: K-Beauty Goes Global: Korea’s Cultural Influence Supports Export Growth

Source: TRASS, BofA Global Research, January 31, 2026.

Source: TRASS, BofA Global Research, January 31, 2026.

Market Dynamics: A Gradual Shift in Participation

Increasing Flows & Participation of Domestic Investors

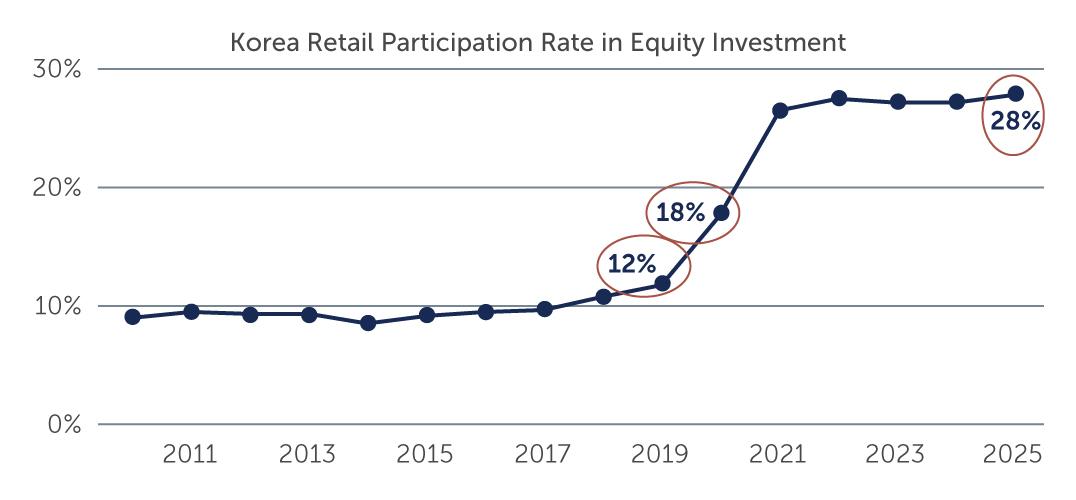

Another important dimension of Korea’s market evolution is the changing composition of its investor base. Historically, the market has been heavily influenced by foreign flows, contributing to periods of volatility and valuation swings. In recent years, however, domestic retail participation has risen notably—particularly since COVID—with individual investors accounting for an increasing share of trading activity and playing a more influential role in market direction.

Policy efforts have increasingly focused on improving market structure and restoring confidence among domestic investors. A key example was the temporary ban on short selling from 2023 to 2025, followed by reforms aimed at reducing the structural disadvantages faced by retail investors relative to institutions—including stricter penalties for illegal activity, enhanced monitoring systems, and more standardized securities lending conditions. Regulators have also broadened the range of investable products, particularly in ETFs, while refining tax and investment frameworks to improve the accessibility and attractiveness of domestic equities.

Taken together, these measures aim to strengthen transparency, fairness, and investor confidence, supporting a more stable and locally anchored investor base. Over time, alongside broader reforms, this could contribute to a gradual shift in household allocation from real estate to equities, reinforcing domestic ownership and supporting potentially more sustainable valuation levels.

Figure 5: Rising Retail Participation in Korea’s Equity Market

Source: Korea Securities Depository, World Bank, Barings, UBS Global Research, May 31, 2026. Retail participation rate is calculated as the number of individual shareholders of Korean listed companies as a percentage of Korea’s total population.

Source: Korea Securities Depository, World Bank, Barings, UBS Global Research, May 31, 2026. Retail participation rate is calculated as the number of individual shareholders of Korean listed companies as a percentage of Korea’s total population.

Valuations After a Stellar Run

Earnings Upgrades Support Further Upside Potential

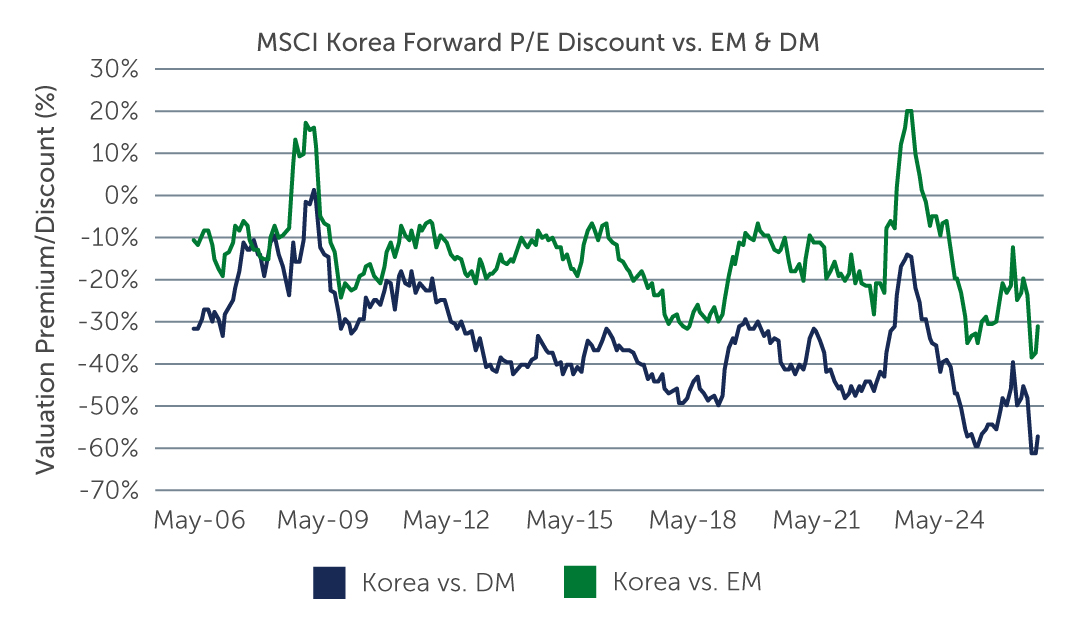

Despite the strong rally since 2025, Korean equities continue to trade at attractive valuations relative to developed markets and key Asian peers. This reflects not only legacy concerns behind the “Korea Discount,” but also continued re-rating momentum in the near-term, supported by upward earnings revisions—particularly within the technology sectors amid the AI-driven cycle. While some moderation in market momentum would be unsurprising after such a strong run, we do not believe the broader structural investment case is deteriorating.

Looking ahead, as earnings visibility improves and governance reforms take hold, there may still be room for valuations to re-rate. This process is unlikely to be uniform, reinforcing the need for a selective and diversified approach to capturing opportunities within Korean equities.

Figure 6: Korea Equities Trade at Discounts Relative to Both Emerging and Developed Equity Markets

Source: MSCI, Refinitiv, Barings, May 31, 2026. EM is measured by MSCI Emerging Market Index, DM is measured by MSCI World Index.

Source: MSCI, Refinitiv, Barings, May 31, 2026. EM is measured by MSCI Emerging Market Index, DM is measured by MSCI World Index.

Conclusion

Korean equities are entering a meaningful period of transition. A market once viewed primarily through a cyclical lens is increasingly being reshaped by technology leadership, policy reform, and a broader set of growth opportunities.

Structural growth in areas such as AI and advanced technology manufacturing is contributing to a stronger earnings foundation, while initiatives aimed at improving corporate governance are introducing a potential re-rating dynamic. At the same time, the opportunity set is broadening across sectors and company sizes.

Rather than being driven by a narrow set of factors, Korea today presents a multi-dimensional investment case. For investors willing to look beyond the headline names, the depth and breadth of opportunities make Korean equities an increasingly relevant component of global portfolios.

1. Source: Company data, BofA Global Research, April 10, 2026.

26-5550230