High Yield Holding Firm as Opportunities Evolve

High yield bonds and loans remain well supported by resilient fundamentals and strong demand, with attractive all-in yields continuing to drive investor interest even as spreads remain tight. At the same time, rising dispersion continues to reinforce the importance of disciplined credit selection and a focus on higher-quality opportunities.

High yield markets remain firmly supported by a strong technical backdrop and a macro environment that has proven more resilient than expected. Demand continues to outpace supply, helping to sustain valuations even as markets navigate ongoing economic and geopolitical crosscurrents.

This dynamic has been a key driver of performance, keeping spreads near historically tight levels and reinforcing the broader stability of the asset class.

At the same time, economic conditions have held up better than many anticipated.

- In the U.S., growth continues to be supported by steady consumer activity, ongoing investment—particularly tied to AI-related infrastructure—and a labor market that remains broadly stable.

- Europe has also shown resilience in the near term, though longer-term questions around competitiveness and industrial demand remain.

Macro risks have not disappeared, but their influence has moderated. Earlier concerns around inflation and energy prices have eased somewhat—although oil markets remain sensitive to geopolitical developments—while the outlook for monetary policy has become more balanced, with fewer rate hikes priced in than earlier in the year. Against this backdrop, high yield bonds and loans remain well supported.

Fundamentals: Resilient, but Increasingly Differentiated

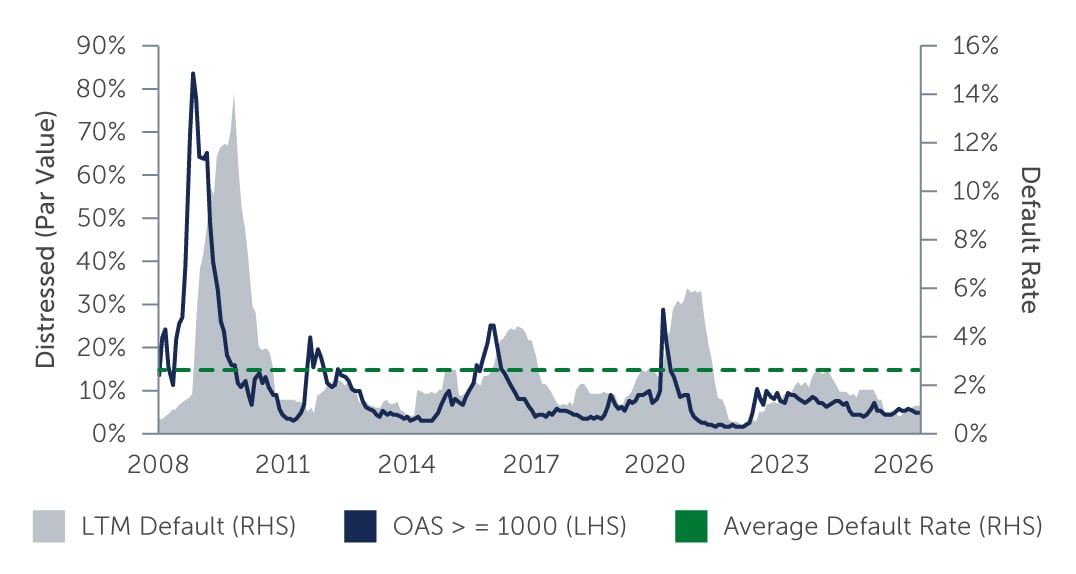

High yield fundamentals remain solid. Corporate borrowers have largely navigated lingering inflation pressures and higher financing costs, and defaults continue to be concentrated in idiosyncratic or issuer-specific situations. Average default rates remain broadly in line with historical averages, while distressed ratios suggest limited systemic stress in the market (Figure 1).

This resilience is supported in part by the higher-quality composition of today’s high yield market, which has a meaningfully larger share of BB issuers relative to history, providing an additional cushion against broad-based deterioration.

Figure 1: Distress Ratio Indicates the Market is not Pricing in Significant Default Activity

Sources: ICE BofA Developed Markets Non-Financial High Yield Constrained Index (HNDC), UBS. As of June 30 2026. Par default rates represent 75% U.S. Default Rate and 25%. European Default Rate.

Sources: ICE BofA Developed Markets Non-Financial High Yield Constrained Index (HNDC), UBS. As of June 30 2026. Par default rates represent 75% U.S. Default Rate and 25%. European Default Rate.

Beneath that stability, however, dispersion is building.

- In Europe, sectors such as chemicals and industrial companies face growing competitive pressure, particularly from China, raising concerns about longer-term earnings erosion. Construction-related activity is showing early signs of recovery, but from a low base and with limited visibility.

- In the U.S., structural questions are emerging in areas such as cable—where competitive pressures from fixed wireless, fiber buildout, and new technologies are affecting long-term growth expectations—and software, where the implications of AI adoption remain highly uncertain.

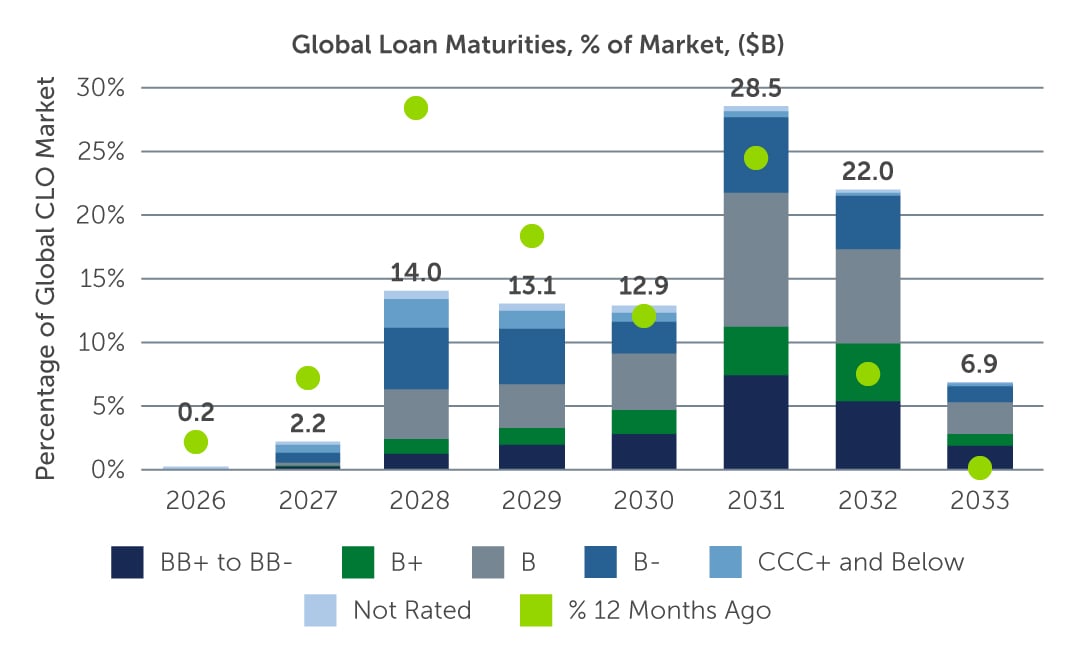

Refinancing dynamics in the primary markets could also become more varied at the issuer level. However, while there is increasing focus on 2028 maturities, the size of that maturity wall has been declining as issuers take advantage of receptive market conditions to proactively extend debt. In fact, over the past year, outstanding 2028 maturities in the global loan market have been reduced significantly—by nearly half compared to 12 months ago. Looking ahead, current market conditions remain supportive for this trend to continue.

Figure 2: Refinancing Risk Remains Manageable

Source: S&P UBS Global Leveraged Loan Index. As of June 30, 2026.

Source: S&P UBS Global Leveraged Loan Index. As of June 30, 2026.

Technicals Remain a Dominant Force

The technical backdrop continues to be shaped by a persistent supply/demand imbalance.

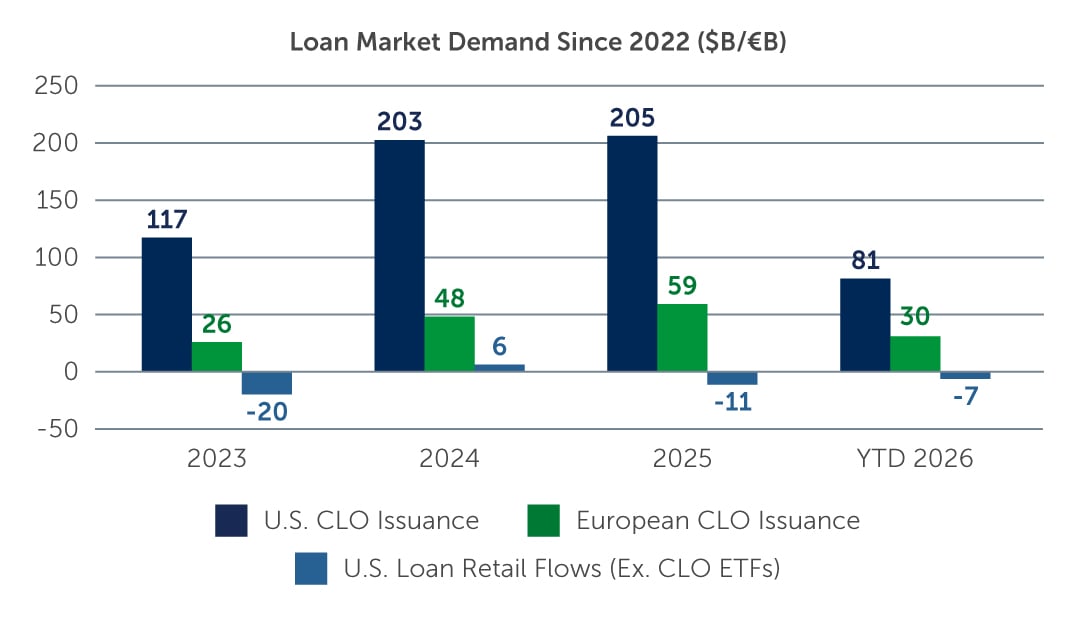

Strong global investor demand has readily absorbed new issuance across both bonds and loans. In loans in particular, CLO formation remains a dominant and highly supportive driver of demand, helping to keep spreads tight across rating cohorts.

Periods of spread widening have generally been met with strong demand, reflecting significant capital available to be deployed and a limited pipeline of net new supply—factors that should continue to limit the potential for sustained widening in the near term.

Figure 3: CLO Demand Remains a Key Driver of Loan Market Technicals

Source: J.P. Morgan. CLO issuance based on new issue transactions and excludes refinancing and reset transactions. CLO ETF flows are positive year to date with over $6.0 billion net inflows. As of June 30, 2026.

Source: J.P. Morgan. CLO issuance based on new issue transactions and excludes refinancing and reset transactions. CLO ETF flows are positive year to date with over $6.0 billion net inflows. As of June 30, 2026.

This demand backdrop has absorbed even thematic surges in issuance. One notable example is the rapid growth of data center-related financing tied to AI infrastructure. While this segment is attracting significant capital, it also introduces new underwriting challenges, including uncertainty around long-term demand, residual values, and evolving technology risks.

Despite these complexities, the broader technical environment remains strong. Limited net new issuance continues to support spreads and valuations across the asset class, even as investors grow more selective at the margin.

Shifting Opportunity Set

Against this backdrop, the nature of opportunity in high yield has shifted.

With spreads tight and broad market upside limited, returns are increasingly driven by income and issuer selection. Avoiding downside, rather than relying on broad market beta, is becoming a defining driver of performance.

In this environment, the opportunity set is increasingly defined by:

- Emphasis on higher-quality credits, including BB bonds and loans that can provide opportunities to capture strong income with greater downside resilience

- Selective exposure to idiosyncratic, lower-rated credits, which require careful underwriting and issuer-specific analysis

- Greater caution toward single-B segments, where valuations have become increasingly compressed, limiting margin for error

Sector dynamics are also evolving. After a period of strong performance, energy appears less compelling on a relative basis, while areas benefiting from more stable or improving input costs—such as packaging and select consumer segments—may offer more balanced risk-reward opportunities.

At the same time, AI remains both an opportunity and a risk. While demand for compute infrastructure is clearly expanding, differentiation between durable business models and more speculative exposures is becoming increasingly important.

Bonds vs. Loans: Relative Value Is Shifting

Both high yield bonds and leveraged loans continue to offer attractive income, but relative value is beginning to diverge.

- Loans continue to benefit from strong technical support—particularly from CLO demand—and attractive carry, but this strength has also compressed spreads in ways that limit upside from current levels.

- High yield bonds, by contrast, offer a more balanced risk-return profile. With duration still modest at around three years, bonds provide potential upside in a scenario where rate expectations continue to moderate. To that end, we believe the bar for further rate hikes is higher than consensus would suggest, particularly as inflation appears to have reached a near-term peak, which could make duration increasingly supportive of returns.

As a result, bonds currently appear more compelling on a relative-value basis, particularly in higher-quality segments where income can be captured alongside potential price appreciation. Opportunities in loans remain increasingly issuer-specific.

What We're Watching Next

The outlook for high yield is broadly constructive. Resilient growth, solid corporate fundamentals and persistent demand for credit continue to provide a strong foundation.

That said, tight spreads may also be masking a gradual increase in dispersion—across sectors, regions and individual issuers. As refinancing risks build and structural challenges emerge in select industries, the margin for error is narrowing.

In this environment, success is less about market direction and more about disciplined fundamental analysis. Generating returns will depend on capturing income, identifying relative value and—importantly—avoiding credits where underlying risks are beginning to surface.

26-5731600