CLOs: Opportunity Amid Growing Dispersion

Dispersion and volatility have reshaped relative value across the CLO market. Structural protections and floating‑rate exposure remain supportive, but outcomes increasingly depend on credit underwriting, manager discipline and an ability to navigate a more selective opportunity set.

After a strong start to the year, markets have shifted. January’s spread compression—driven by a constructive technical backdrop—has given way to renewed volatility amid the war in Iran, AI‑related disruption and heightened scrutiny across private credit. At the same time, inflation has proven more persistent than expected, reinforcing a higher‑for‑longer rate environment and resetting expectations across credit markets.

In the CLO market, this backdrop has resulted in more pronounced dispersion across the capital structure. Senior tranches have generated positive year‑to‑date returns, underscoring the value of structural protection and floating‑rate income. Lower‑rated tranches have experienced more volatility, reflecting greater sensitivity to loan prices and tail risks. Importantly, wider spreads have also created more attractive entry points in certain segments, reinforcing a more constructive, but selective, outlook for investors focused on relative value and risk management.

Fundamentals: Intact, With Greater Dispersion

From a fundamental standpoint, CLOs continue to benefit from generally stable conditions in the leveraged loan market. Many issuers entered the year with adequate interest coverage and cash flow generation, providing a buffer against slowing growth and tighter financial conditions.

However, dispersion across issuers and sectors has increased:

- Higher rates have delayed deleveraging and elevated refinancing risk for loans with nearer‑term maturities. This is most evident in interest-rate sensitive sectors like housing, where expected relief from rate cuts has been pushed out.

- Credit outcomes are becoming more issuer‑specific. Exposure to technology, and the potential for AI‑driven disruption, has come under closer scrutiny, driving meaningful divergence within sectors.

- Maturity profiles are a factor. Loans approaching 2027–2029 refinancing windows are receiving greater attention, particularly where sector headwinds could limit capital market access.

As dispersion increases, fundamental analysis at the issuer level—focused on cash‑flow durability, business model resilience and refinance visibility—has become increasingly important in shaping collateral quality within CLO portfolios.

Technicals: Supportive, But Uneven

Technical conditions are playing a prominent role in shaping performance. Returns have become more bifurcated across the capital structure, with senior tranches benefiting from sustained demand for quality and liquidity, while mezzanine tranches—especially BBs—have been more sensitive to loan price volatility

Wider liabilities have pressured new issue equity arbitrage, contributing to slower new issuance, and portfolio clean-up requirements are resulting in fewer resets. This slowdown has reinforced technical support for the asset class overall, even as regulatory developments reinforce differentiation—with higher rated tranches positioned to benefit relative to mezzanine over time.

Opportunities Across the Capital Structure

Relative value across the CLO capital structure has become more nuanced, with dispersion creating opportunity rather than signaling broad deterioration. In the months ahead, flexibility—between primary and secondary markets, regions, and public versus private credit structures—will be an important source of potential value.

At the top of the capital structure:

- AAA and AA tranches remain compelling for investors seeking durable income supported by strong structural protections

- Recent spread widening has enhanced carry, particularly relative to where valuations stood earlier in the year

- Floating‑rate coupons continue to benefit from a higher‑for‑longer rate environment

- Secondary markets often offer more compelling relative value than new issuance, given ample supply—particularly in U.S. AAA tranches

Mezzanine opportunities are increasingly selective, reflecting the growing role of dispersion and tail‑risk sensitivity:

- BBBs have become a focal point for differentiation, with outcomes more heavily influenced by collateral composition and manager behavior.

- BBs have absorbed more of the recent volatility, reflecting their sensitivity to loan price declines.

- Spread widening has weighed on near-term performance, but it has also resulted in more attractive valuations for higher‑quality mezzanine deals with limited tail risk.

- Across mezzanine, rigorous credit analysis and careful manager selection are essential.

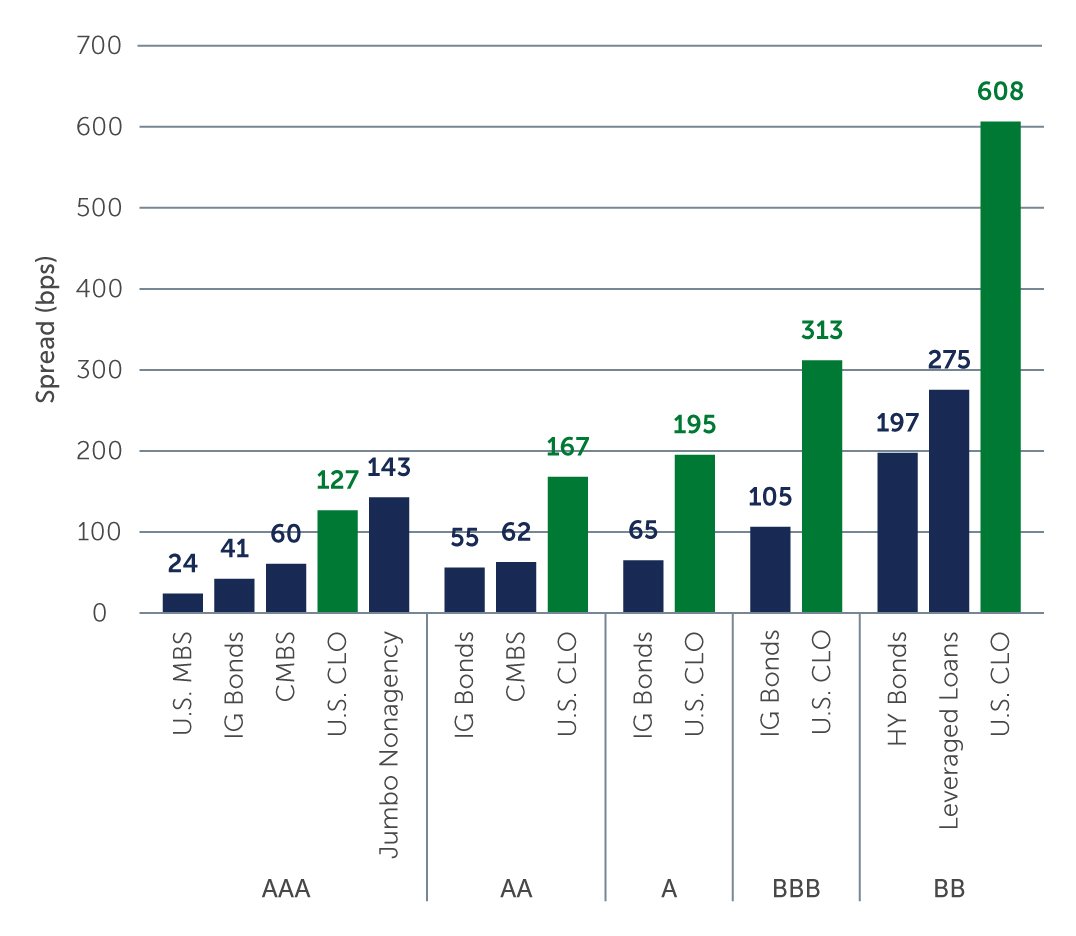

Figure 1: Spreads by Rating

Sources: J.P. Morgan U.S. CLO Spreads; BofA Global Research Jumbo Nonagency Spreads; Bloomberg U.S. Aggregate Index—CMBS & Corporate IG; Bloomberg U.S. Corporate High Yield Index; S&P UBS Leveraged Loan Index; Barings. As of March 31, 2026. Note: Represents new issue CLO spreads.

Sources: J.P. Morgan U.S. CLO Spreads; BofA Global Research Jumbo Nonagency Spreads; Bloomberg U.S. Aggregate Index—CMBS & Corporate IG; Bloomberg U.S. Corporate High Yield Index; S&P UBS Leveraged Loan Index; Barings. As of March 31, 2026. Note: Represents new issue CLO spreads.

CLO equity opportunities remain more episodic but can become attractive during dislocations. Challenged arbitrage has weighed on new issue formation, but periods of volatility can still create selective opportunities—most often through discounted secondary equity positions and, in some cases, through primary issuance when loan prices temporarily dip and allow managers to quickly ramp a lower-priced asset portfolio.

Private Credit CLOs: A Reset in Relative Value

Private credit CLOs have also moved back into focus following a period of spread widening driven by negative headlines, redemption activity and broader scrutiny of private markets. While fundamentals in the underlying collateral have not deteriorated materially, sentiment has shifted, pushing spreads wider and reopening a relative value opportunity that had been less pronounced in recent quarters. As with broadly syndicated CLOs, selectivity remains critical, with transparency into underlying credit, portfolio construction and manager behavior taking on heightened importance amid the ongoing attention on private credit more broadly.

What’s Next?

The CLO market has entered a more selective phase, shaped by wider dispersion across credits and capital structures. While macro uncertainty remains elevated, performance has been uneven rather than broadly challenged.

Key themes likely to shape outcomes include:

- Refinancing timelines and maturity profiles

- Sector‑specific pressures, particularly in interest and disruption-sensitive areas

- Active credit management and disciplined portfolio construction

Overall, the outlook for CLOs is constructive but selective. Wider spreads have improved entry points, but success in this environment will depend not only on the macro backdrop, but also—increasingly—on credit and manager selection, alongside active risk management.

26-5391608