IG Credit: Strong Fundamentals, But Inflationary Pressures Grow

Current yield and spread levels, coupled with companies’ durable credit profiles, suggest that IG corporate credit continues to look attractive—but a number of risks remain on the horizon.

Rising costs began to pare down investment grade (IG) corporate margins from historical highs in the third quarter, while a second consecutive 75 basis points (bps) interest rate hike reaffirmed the U.S. Federal Reserve’s (Fed) aggressive stance on fighting inflation. The ongoing war in Ukraine, lingering supply chain issues and growing labor costs further weighed on sentiment, fueling fears of an economic “hard landing” or recession. At the same time, the U.S. dollar strengthened, further complicating profit outlooks for IG companies. All of these factors contributed to the growing risk-off tone in the market, which led to a negative total return for IG corporate bonds, with the asset class down -5.06% at quarter-end.1 On a sector basis, financials underperformed industrials, while utilities outperformed, in keeping with the rotation into defensive sectors.

While spreads tightened marginally during the quarter, they remain wide relative to five and 10-year averages. At the same time, yields have climbed rapidly—the IG corporate index is currently yielding around 5.69%, mostly driven by higher rates.2 These current yield and spread levels, coupled with issuers’ durable credit profiles, suggest that IG corporate credit continues to look attractive from a valuation perspective relative to the past 12–24 months.

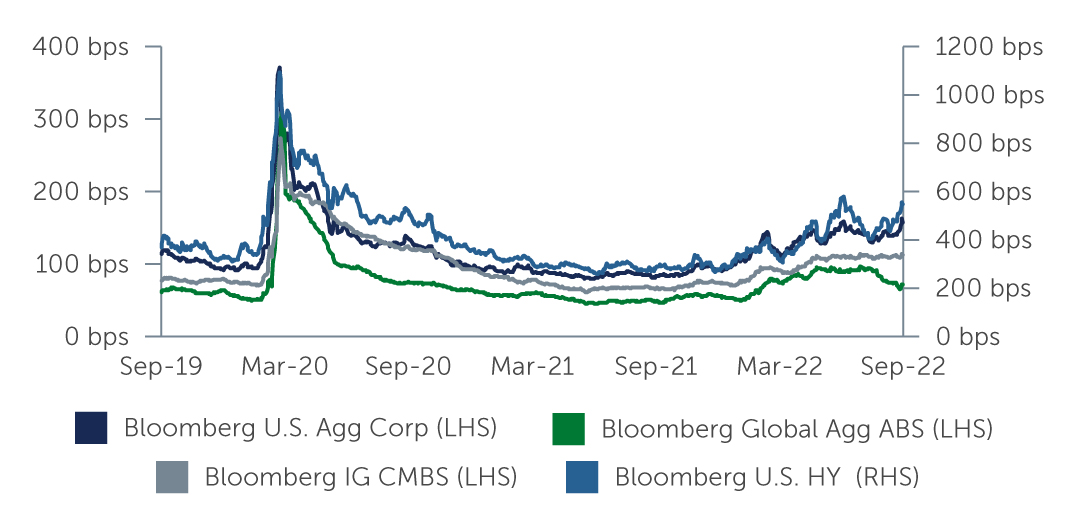

Figure 1: IG Valuations Look Potentially Attractive

Source: Bloomberg Barclays. As of September 30, 2022.

Source: Bloomberg Barclays. As of September 30, 2022.

Inflation Woes Test Fundamentals

Revenues and earnings began the third quarter at relative strength with strong year-over-year growth, though early indications point to some erosion in fundamentals due to inflation. Profit margins have declined from previous quarters due to higher energy and labor costs, as well as the effect of currency changes amid a strengthening U.S. dollar. On the positive side, leverage levels continued to tick down. As corporate debt levels have decreased, interest expenses have come down as well. At the same time, interest coverage has increased, helping maintain accumulated balance sheet strength.

Technicals Remain Mixed

The upward rate trend and subsequent negative returns have resulted in further outflows from the asset class, despite several weeks of inflows during the summer. However, higher rates have also led to lighter-than-expected supply as companies delay issuing new bonds, adding some technical support. The decline in anticipated new issues should remain supportive of the asset class through the remainder of the year, and demonstrates the ability of IG companies to manage through the tightening cycle without increasing leverage.

Interestingly, despite the recent spike in yields, demand from yield-seeking overseas investors has been less than expected, largely due to high currency hedging costs. That said, certain non-hedged vehicles, such as U.S. dollar-denominated products, continue to see some demand, particularly from buyers in Asia.

Wider Spreads Leading to Opportunities

As spreads have remained wide relative to recent history—particularly the period of post-COVID spread compression that continued through 2021—we are finding potentially attractive buying opportunities in several areas of the market where spreads have widened beyond what fundamentals would suggest. From a sector perspective, we continue to find value in financials, a sector that has recently underperformed. New issues, some with sizeable concessions, from larger U.S. money center banks, regional banks, and banks in Asia and Europe have provided compelling opportunities, particularly in shorter-duration credits. We also see value in select, less-liquid companies in the financial sector—such as business development corporations, air lessors, asset managers and smaller insurance companies—that have fallen out of favor amid recent volatility, despite having strong credit profiles that should support performance going forward. We also continue to find opportunities in the energy sector. Cash flows remain solid even as oil and natural gas prices have moderated from their highs. With a number of existing bonds expected to be called or tendered soon, the sector continues to exhibit compelling new issue supply/demand dynamics.

Outside of traditional IG corporate credits, spreads have widened on certain securitized products such as mortgage CRTs, creating the potential for significant spread pick-up. In particular, we see attractive opportunities in issues with solid cash flows and high credit ratings, especially as consumer balance sheets have remained healthy. High-rated AAA CLOs also offer the potential for a significant spread pick-up, with the added benefit of robust structures that have helped the asset class weather past periods of volatility well. Consistent with opportunities in IG corporates, shorter duration assets look more appealing amid widening spreads and economic uncertainties.

What’s Next

The risks that drove investor sentiment earlier this year remain in play today. The Russia-Ukraine war continues to cause economic and political uncertainty. The Fed’s hard stance on inflation has increased fears that rate tightening will lead to a recession or to stagflation—an inflationary environment paired with weak economic growth. We continue to watch any indication of ebbing inflation and a possible softening of the Fed’s hawkish policies that could reduce the heightened rate volatility. Additionally, we are monitoring corporate earnings for signs that the economy has reached recessionary inflection points.

Earnings warnings from bellwether companies FedEx and Ford indicate that recessionary fears and the impacts of inflation will continue to put pressure on corporate revenues, supply chains and consumer sentiment, which could meaningfully impact demand. Against this backdrop, we anticipate spreads may have further room to widen, even if corporate fundamentals remain largely intact. While corporate debt has held up well and outperformed equity, a prolonged decline in equities will result in a difficult environment for corporate fixed income. Negative performance resulting in further outflows may create additional technical headwinds.

In this environment, bottom-up credit selection remains key, not only to identifying and capitalizing on opportunities, but also to managing—and mitigating—the myriad of current risks that could impact the asset class going forward.

1. Source: Bloomberg Barclays. As of September 30, 2022.

2. Source: Bloomberg. As of September 30, 2022.

22-2461526