Looking Inside Today’s High Yield Market

High yield investors are navigating a more complex backdrop, but fundamentals remain resilient and income continues to look compelling. Markets have absorbed a steady stream of risk events, but the environment calls for discipline rather than complacency.

The Backdrop: Volatility Without Capitulation

The year began with expectations of a supportive growth and policy mix, but conditions shifted quickly.

- Geopolitical risk has moved to the forefront, with the war in Iran creating volatility in energy prices and reintroducing uncertainty around inflation and global growth.

- AI and software repositioning remain considerations, but have taken a back seat to broader macro questions tied to geopolitics and policy.

- Regional dynamics are diverging. Europe appears structurally more sensitive to energy‑driven inflation and policy constraints, while the U.S. is more exposed to technology‑linked shifts in sentiment.

Against this backdrop, high yield bonds and loans have held up well. Rather than broad capitulation, markets have experienced pockets of weakness, with spreads widening only incrementally relative to the scale and frequency of headline risk. This reflects a market that remains cautious but reluctant to aggressively reduce exposure—consistent with an economic backdrop that has so far proven resilient despite recurring risk events.

Fundamentals: Stable, with Pockets of Stress

High yield fundamentals are on solid footing, even as the macro environment has become more unsettled.

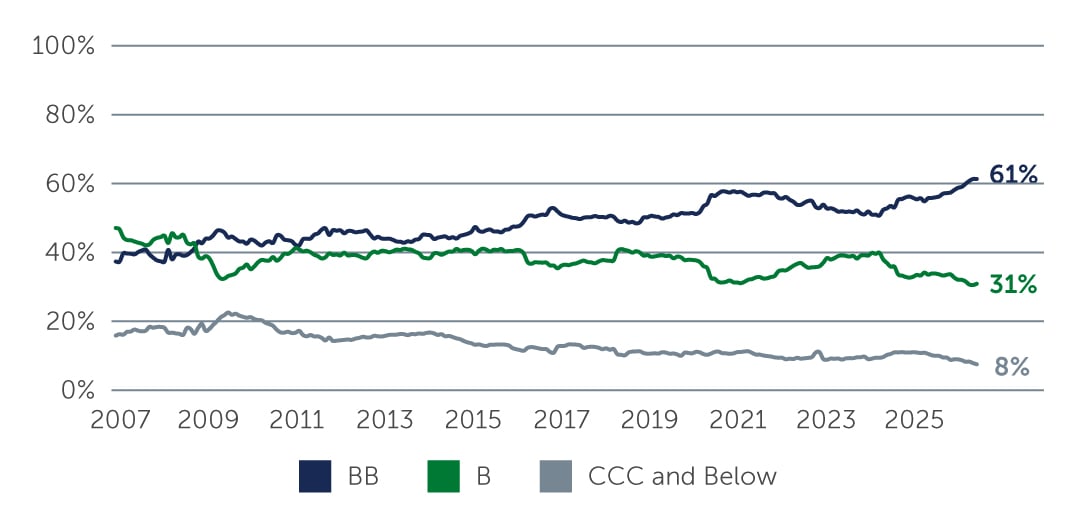

- Today’s market reflects a higher‑quality credit mix than in prior cycles, with BB issuers making up a large share of the opportunity set and relatively limited exposure to the most stressed CCC segments (Figure 1). This composition has helped support overall market stability and should continue to provide a buffer against volatility.

- Earnings have generally held up, supported by resilient end demand and companies’ continued pricing power.

- Balance sheets remain supported by manageable interest burdens and leverage levels.

Figure 1: The HYB Market is Higher-quality Relative to History

Source: ICE BofA Non-Financial Developed Markets High Yield Constrained Index. As of March 31, 2026.

Source: ICE BofA Non-Financial Developed Markets High Yield Constrained Index. As of March 31, 2026.

That said, dispersion is increasing.

- Some cyclical sectors, including building materials and chemicals, are showing strain after taking on higher leverage during periods of heavy M&A activity.

- In the U.S., select software issuers remain under scrutiny as competitive pressures persist and the market works to price in potential AI-related risks to long-term business models.

Even so, these areas represent a modest share of the overall high yield market, limiting their impact at the index level.

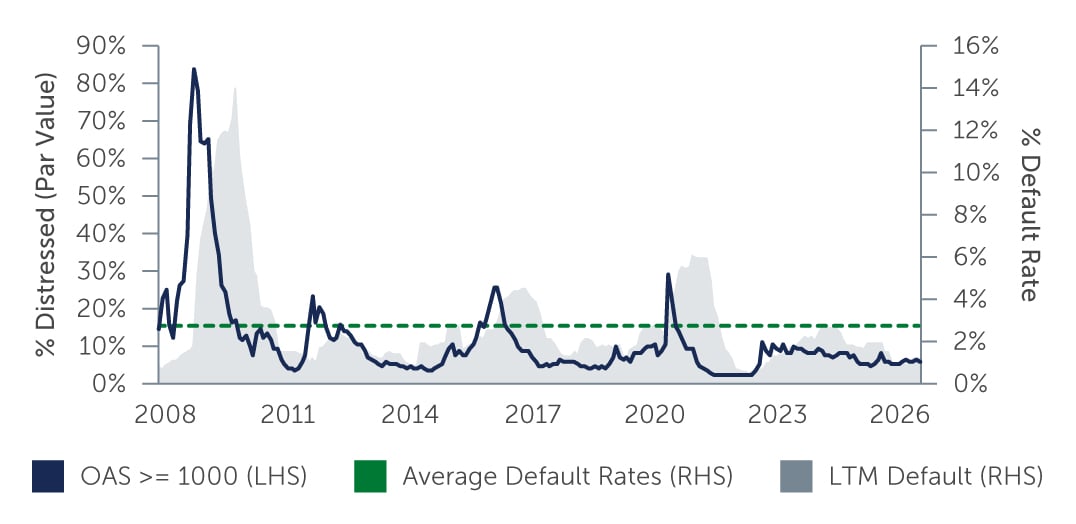

Looking ahead, default expectations remain broadly stable. Distress indicators across bonds and loans continue to point to default rates that are in line with recent levels and below long‑term averages (Figure 2). While an uptick cannot be ruled out, any increase would occur from a low starting point and is likely to be offset by current income levels.

Figure 2: The HYB Market is Not Pricing in Significant Default Activity

Source: ICE BofA Developed Markets Non-Financial High Yield Constrained Index; UBS. As of March 31, 2026.

Source: ICE BofA Developed Markets Non-Financial High Yield Constrained Index; UBS. As of March 31, 2026.

Technicals: Balanced Despite Shifting Ownership

Market technicals have proven more resilient than headlines suggest. Primary markets remain open for both bonds and loans, with new issuance coming at levels that have improved entry points without disrupting overall market stability.

A notable feature of the current environment has been the evolving interplay between public and private credit markets. While redemptions in certain non‑traded private credit vehicles have raised concerns about potential spillover into liquid markets, we have not seen forced selling, nor is there evidence that broadly syndicated loan performance has been negatively affected. In fact, year-to-date performance for syndicated loans improved in March (Figure 3). Rather, the impact has been more subtle—for instance, private credit vehicles that have historically stepped in as marginal buyers during periods of volatility have been less consistent sources of demand.

Figure 3: Year-to-Date Broadly Syndicated Loan Market Performance Improved in March

Sources: Barings; S&P UBS Global Leveraged Loan Index. As of March 31, 2026.

Sources: Barings; S&P UBS Global Leveraged Loan Index. As of March 31, 2026.

In loans, CLO behavior remains central. With CLOs dominating both ownership and incremental demand, pricing has become increasingly sensitive to eligibility considerations tied to ratings, sectors and deal structures. This has led to sustained pressure on certain single‑B and CCC loans, pushing prices lower at times than what fundamentals would suggest is fair. While these dynamics have created greater dispersion, they largely reflect structural constraints rather than broad credit deterioration.

Where Opportunities Are Emerging

Against a backdrop of uneven repricing across credit markets, opportunities are increasingly shaped by relative value, capital structure positioning, and credit selection rather than broad market exposure. Recent market resilience has reduced the urgency to add risk indiscriminately, placing a greater premium on patience and selectivity. Both bonds and loans offer attractive attributes, with the most compelling opportunities emerging where recent price moves reflect technical or macro pressures rather than a deterioration in underlying fundamentals.

High Yield Bonds: Quality at Attractive Levels

- Higher government yields and bouts of volatility have pushed all-in yields higher, improving income even in higher-quality segments of the market while still offering relatively modest duration.

- This reset has allowed investors to be more selective, reducing the need to reach down the quality spectrum in search of yield

- BB and select single-B credits stand out, particularly issuers with durable business models, manageable leverage and clear refinancing visibility.

Together, these segments offer an attractive combination of income and downside resilience as markets adjust to ongoing uncertainty, creating opportunities to improve portfolio quality without sacrificing income.

Leveraged Loans: Income and Structural Protection

Loans remain attractive for their senior secured position in the capital structure and floating-rate coupons, which continue to translate into high levels of current income with limited sensitivity to interest rate movements.

In a market shaped by CLO‑driven differentiation, opportunity is increasingly found at the issuer level rather than through broad exposure. Loans that sit outside CLO parameters for structural or eligibility reasons can trade at discounted levels despite stable fundamentals, creating select opportunities for investors able to underwrite credit risk on a case‑by‑case basis.

What’s Next for High Yield

High yield is operating in a more complex environment than anticipated at the start of the year, shaped by geopolitical uncertainty, shifting rate expectations, and sector-specific challenges. While growth—particularly in the U.S.—has remained resilient, inflation risks appear to be building rather than fading, reinforcing rate volatility across fixed‑income markets. Despite these crosscurrents, the market’s core characteristics remain intact: relatively strong credit quality, contained defaults and compelling income.

At the same time, dispersion is rising. The opportunity set going forward is likely to be defined less by broad beta and more by issuer fundamentals and structure-specific outcomes. Maintaining optionality and flexibility is critical. Attractive entry points will likely emerge, but capitalizing on them will require active monitoring, disciplined credit selection, and readiness to deploy capital decisively if volatility translates into clearer market dislocations.

26-5374927